Credit Report Redesign

At Experian Consumer Services, I led the redesign of their digital credit monitoring platform, transforming how millions of consumers interact with their credit information. We evolved the experience from a static, anxiety-inducing platform into a business-scalable system with transparent upsell opportunities that provide genuine value. The platform has set new industry standards for credit information accessibility while creating sustainable revenue streams, with its core features still serving millions of users after four years.

Client:

Experian Consumer Services

Role:

Lead designer

Year:

2021

The Challenge

Our team approached this credit report redesign with extensive research. Working with our research, consumer insights, data science, and optimization teams, we identified what information users needed most and when they needed it. This wasn't just a visual update—it was building a scalable business platform that could evolve with both user needs and business requirements. Our research uncovered several critical barriers:

CHALLENGE 01

The previous design required complete overhauls to incorporate new features or monetization opportunities, severely limiting business scalability and future growth.

CHALLENGE 02

Users viewed credit reporting and upsell moments with deep skepticism, perceiving monetization attempts as predatory rather than value-adding.

CHALLENGE 03

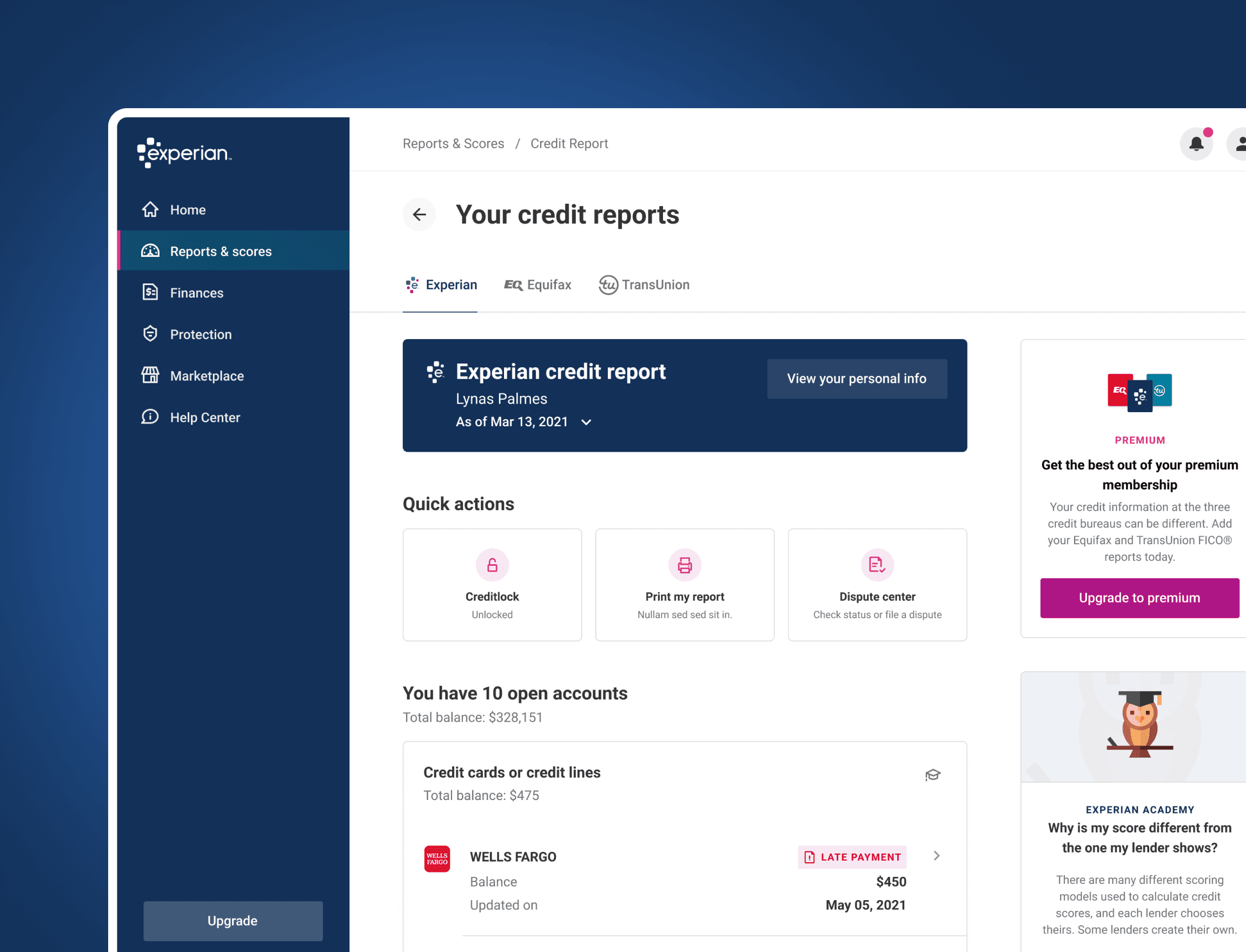

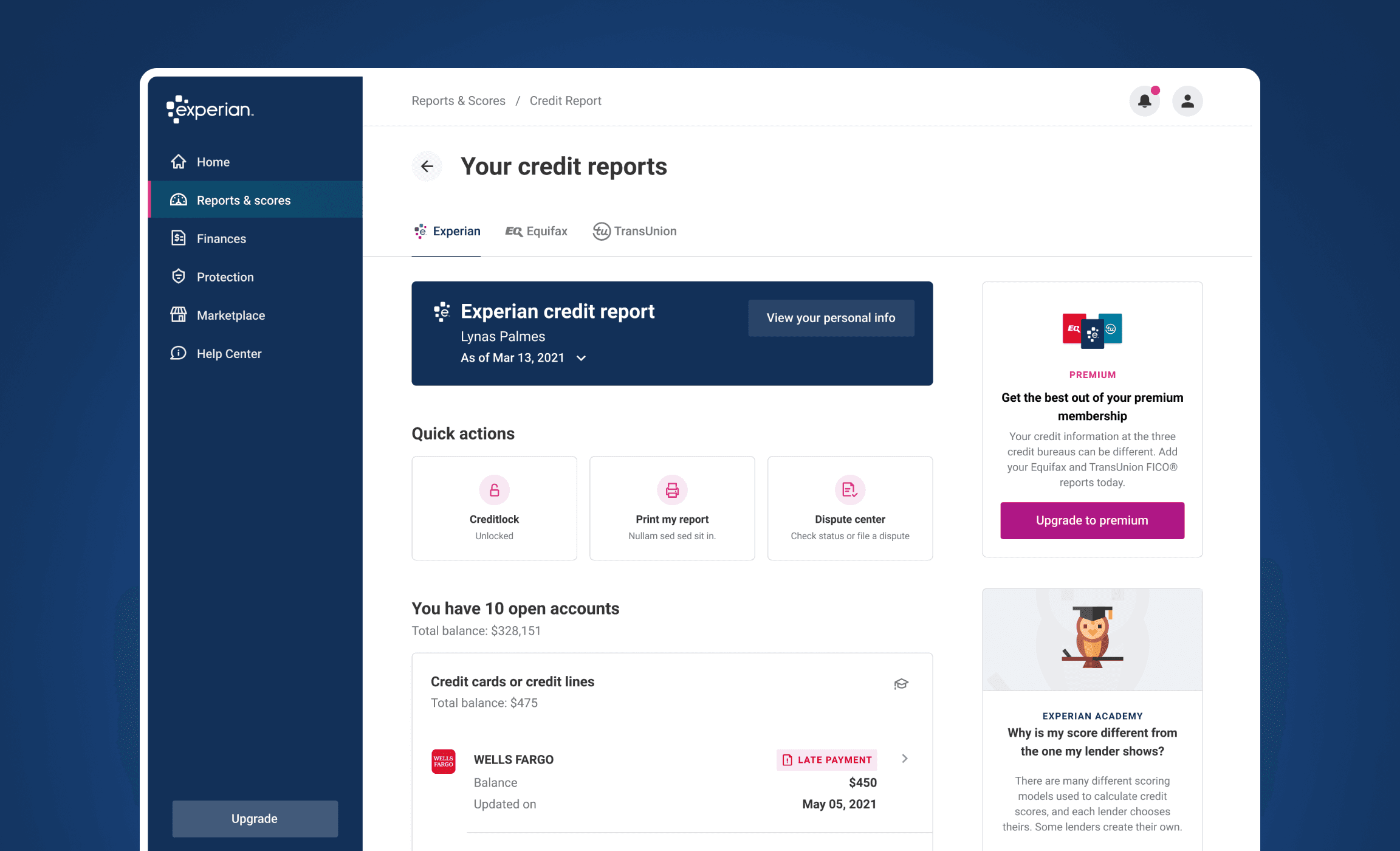

Poor information hierarchy and accessibility. The wide layout with dense information, small text, inadequate spacing, and lack of visual separation between account groupings created accessibility barriers and made it impossible for users to identify critical information or next steps.

CHALLENGE 04

The disconnection between data presentation and actionable next steps created furstration and missed opportunities for both users and the business.

Outcomes

The redesign transformed Experian's credit reporting platform into a user-friendly system that drives business growth through transparent value exchange:

SUSTAINABLE BUSINESS GROWTH

The redesigned platform delivered a 23% increase in free-to-paid conversions while enabling continuous testing and optimization of monetization strategies without requiring full redesigns.

INCREASED USER RETENTION

Users began returning to the platform more frequently, motivated by clear value and actionable insights rather than anxiety, establishing a virtuous cycle of engagement with both free and premium features.

OPERATIONAL EFFICIENCY

Support call volume related to credit report confusion notably decreased post-launch, freeing up customer service staff for more complex issues, while the component architecture dramatically accelerated development cycles for new features from months to weeks.

Process

The credit report redesign was anchored in a methodical approach that balanced user needs with business objectives. Here's how we executed this transformation:

STEP 01

Understand what the problems are

The responsibility of redesigning how 200 million consumers interact with their personal financial data required acknowledging the real-world context: most people only check their credit report when absolutely necessary, and the experience is rarely positive—especially for those facing financial hardship or simply trying to navigate life without constant financial scrutiny.

There was a survey that we had rolled out to consumers, to better understand how people are feeling about the app and if they find it useful. We received and overwhelmingly amount of 100K responses. Here are some of the responses:

“Credit rating companies are a sham. The algorithms used are not accurate and reward the wrong behaviors. I have never missed a payment and payoff all my bills every month, but yet I have a mid 700s score.”

“You send me credit card options every day! Why! My credit score is great because I don't have all the credit cards anymore! Why on earth would you sit here and advertise cards every day to people who might have issues with their credit? Are you in their employ? Are you trying to get people in trouble?”

“I have no choice. I get rated by experian regardless of how I feel about it. Your rating system is cryptic. My credit goes up and down with the wind. And I am not your customer, I am your product that you sell. So I am not sure how I am supposed to recommend you to anybody.“

“You use accounts that are not mine and it does not seem to be consistent or accurate.“

STEP 02

The opportunity to sit down with actual consumers in person was a treat. I was able to connect with consumers on another level and showing clear signs of empathy

Conducted in-depth, in-person sessions with consumers to understand their pain points, observing users interacting with existing credit reports and documenting both emotional responses and functional challenges to build a comprehensive understanding of the user experience barriers.

STEP 03

Iterative usability testing

Created multiple design concepts based on research insights and tested them with real users, refining the experience through successive iterations that addressed identified barriers, bringing us closer to an optimal solution.

STEP 04

I generated various test accounts across different membership tiers to comprehensively analyze how information access varies between user segments, revealing critical gaps and opportunities in the user journey based on membership status that informed our tiered design approach.

Created and analyzed user journeys across free, basic, and premium membership tiers.

Identified information discrepancies and feature access points that caused confusion or frustration.

Mapped emotional touchpoints where users encountered paywalls or limitations.

Analyzed conversion opportunities where users most frequently upgraded memberships.

Evaluated which premium features delivered the most perceived value to different user segments.

Documented differences in data presentation and detail level across membership tiers.

Identified opportunities to enhance value perception at each membership level.

STEP 05

Strategic educational integration

Identified natural moments in the user journey where educational content could provide value without overwhelming users, making financial literacy an organic part of the experience rather than a separate, easily ignored component.

STEP 06

Business-consumer value alignment

Balanced user needs with business goals, ensuring that empowering consumers with better information also created growth opportunities for the company through strategically positioned contextual ads and upsells that provided value at the right moments.

Solution

Solution 01 - Scalable component architecture

We developed a modular design system with standardized components that could be easily updated, rearranged, or expanded as business needs evolved. This narrower, more focused layout improved usability while creating strategic spaces for contextual features and monetization opportunities that could be tested and optimized independently.

Solution 02 - Transparent value exchange

We reimagined how premium features are presented by creating clear, honest connections between user needs and business offerings. Instead of generic and disruptive upsells, we positioned premium features precisely when and where they delivered obvious value, making the business case transparent to users. For example, after showing users potential credit issues, we offered relevant premium tools to address them rather than generic upgrade messaging (Prime example is CreditLock).

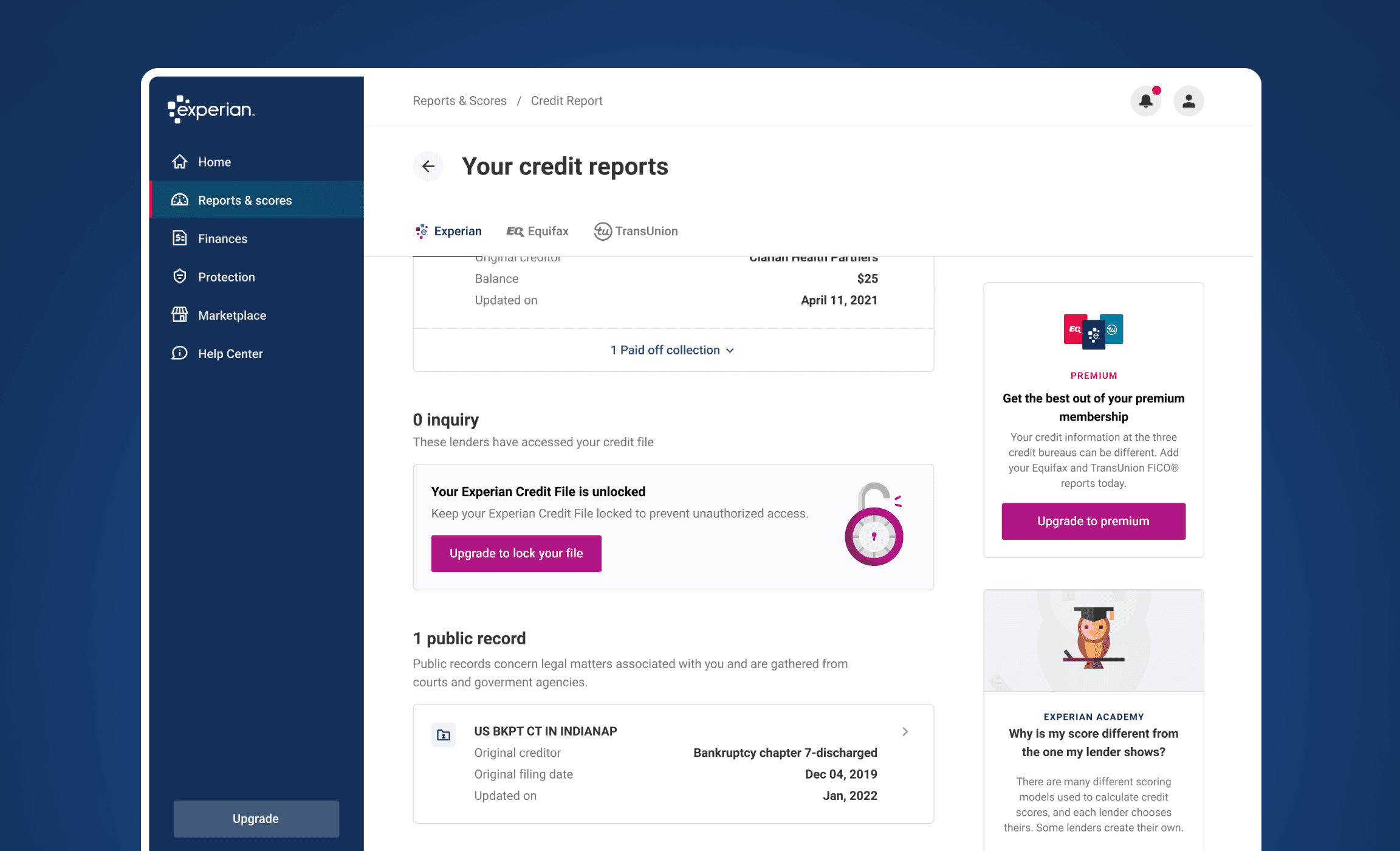

Solution 03 - Pattern-based information architecture

Based on our research findings, we addressed information overload by implementing consistent organizational patterns that break down complex credit data into digestible modules. Rather than hiding account details in dropdowns that obscured important information, we utilized expandable drawer components that reveal comprehensive details while maintaining context. This approach transforms overwhelming credit data into a structured experience with clear visual patterns, helping users quickly recognize account types, status indicators, and critical information without cognitive strain.

Solution 04 - Contextual action framework

We integrated relevant action items directly within the context of each information section, ensuring users always knew what steps they could take based on their credit data. This included both free actions (disputing errors, setting up payment reminders) and premium opportunities, creating a seamless journey from information to action that benefited both users and the business.

Key takeaways

This project uncovered that effective financial tools must address both cognitive and emotional aspects, with my role as lead designer focused on building user confidence through educational elements—a human-centered approach often overshadowed by business metrics and feature discussions.

Checking credit scores is inherently emotional, giving us the responsibility to help users understand and engage with financial information through clarity rather than anxiety.

Our metrics confirmed that successful financial products evolve with users, supporting their journey to healthier financial habits by addressing emotional barriers, knowledge gaps, and trust deficits.