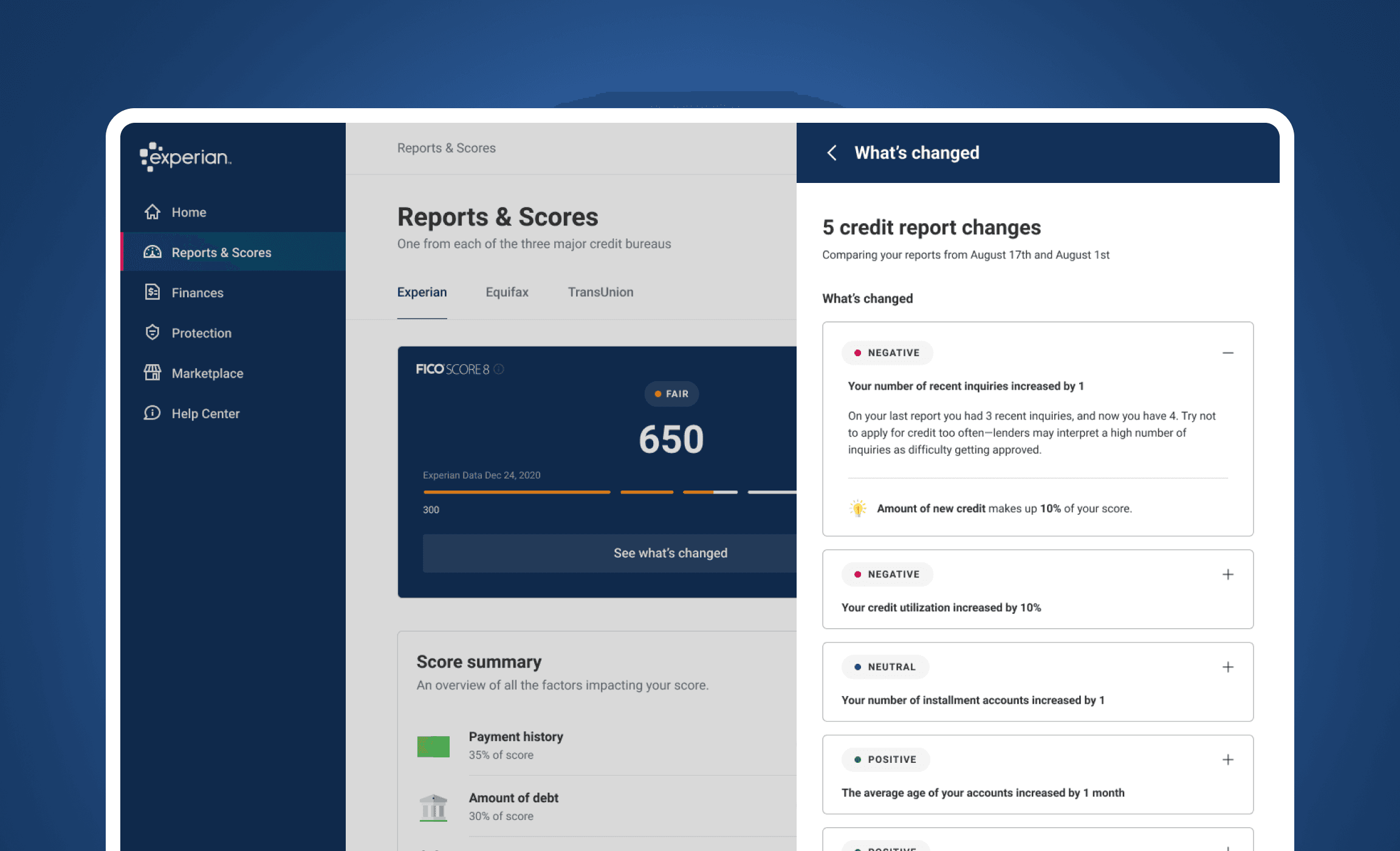

What's changed

The What's Changed feature transformed those confusing, anxiety-inducing moments of unexplained credit score changes into opportunities for clarity and action. By translating complex credit factors into simple, personalized guidance, we helped users understand exactly why their scores changed and what they could do about it. The impact was clear—users finally understood their credit, engaged more with the service, and gained confidence in managing their financial health. What began as a fix for frustrated customers became a trusted companion on their financial journey.

Client:

Experian Consumer Services

Role:

Lead designer

Year:

2021

The Challenge

Users are frustrated with the credit monitoring service due to a lack of transparency when their credit scores change. This has resulted in a low NPS score of 13.

CHALLENGE 01

NPS score of 13 indicates significant user dissatisfaction

CHALLENGE 02

Users report frustration when seeing unexplained credit score changes

CHALLENGE 03

Lack of explanation leads to disengagement with the service

Outcomes

We tested the 'What's Changed' feature with a controlled user group before full deployment, showing positive outcomes. The success metrics from the test group validated the approach, providing confidence to proceed with a full rollout to all users.

USER COMPREHENSION

80% of users reported significantly improved understanding of score changes and necessary actions

STRONG FEATURE ENGAGEMENT

30% engagement rate demonstrated regular interaction with the feature

IMPROVED CUSTOMER SUCCESS SATISFACTION

NPS increased by +4 points

Process

STEP 01

Strategic framework development

For the 'What's Changed' project at Experian, we used behavioral economics—a field that combines psychology and economics to understand how people make real-world decisions, recognizing that humans are influenced by cognitive biases, emotions, and social factors rather than always acting rationally. We discovered that users experience disproportionate anxiety even with small score decreases—this is called 'loss aversion,' where people feel losses more strongly than equivalent gains.

This insight was crucial because it showed us that the technical problem (explaining credit score changes) was actually an emotional problem. Users weren't just confused—they were anxious and frustrated when seeing unexplained changes.

Our framework had three key principles:

Transform anxiety into action by providing context for changes

Reframe negative experiences to feel less threatening

Reduce cognitive load when explaining complex credit factors

By approaching the problem this way, we could design solutions that addressed both the technical need for information and the emotional need for reassurance and clear direction.

STEP 02

Credit data translation

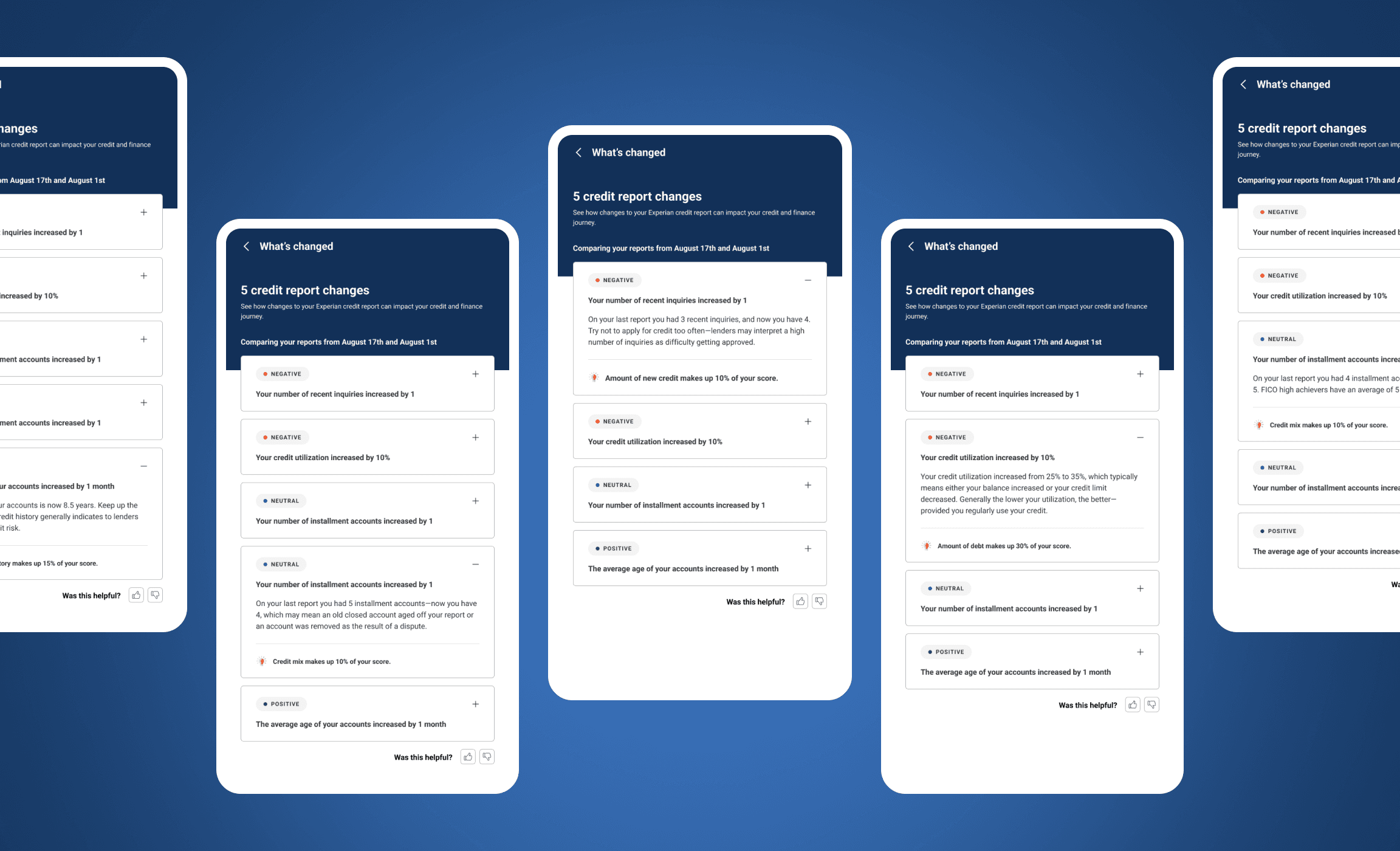

It was important to understand the complex credit data so that I could decode it and turn it into user-friendly language. The process for this was analyzing FICO patterns and utilize user feedback to bridge the gap between technical and credit reporting and practical consumer understanding.

Our detailed analysis of 15+ credit factors (including payment history, account age, and utilization rates) enabled us to create a system that could identify changes, calculate relative impact, and generate personalized explanations.

STEP 03

User resarch and insight development

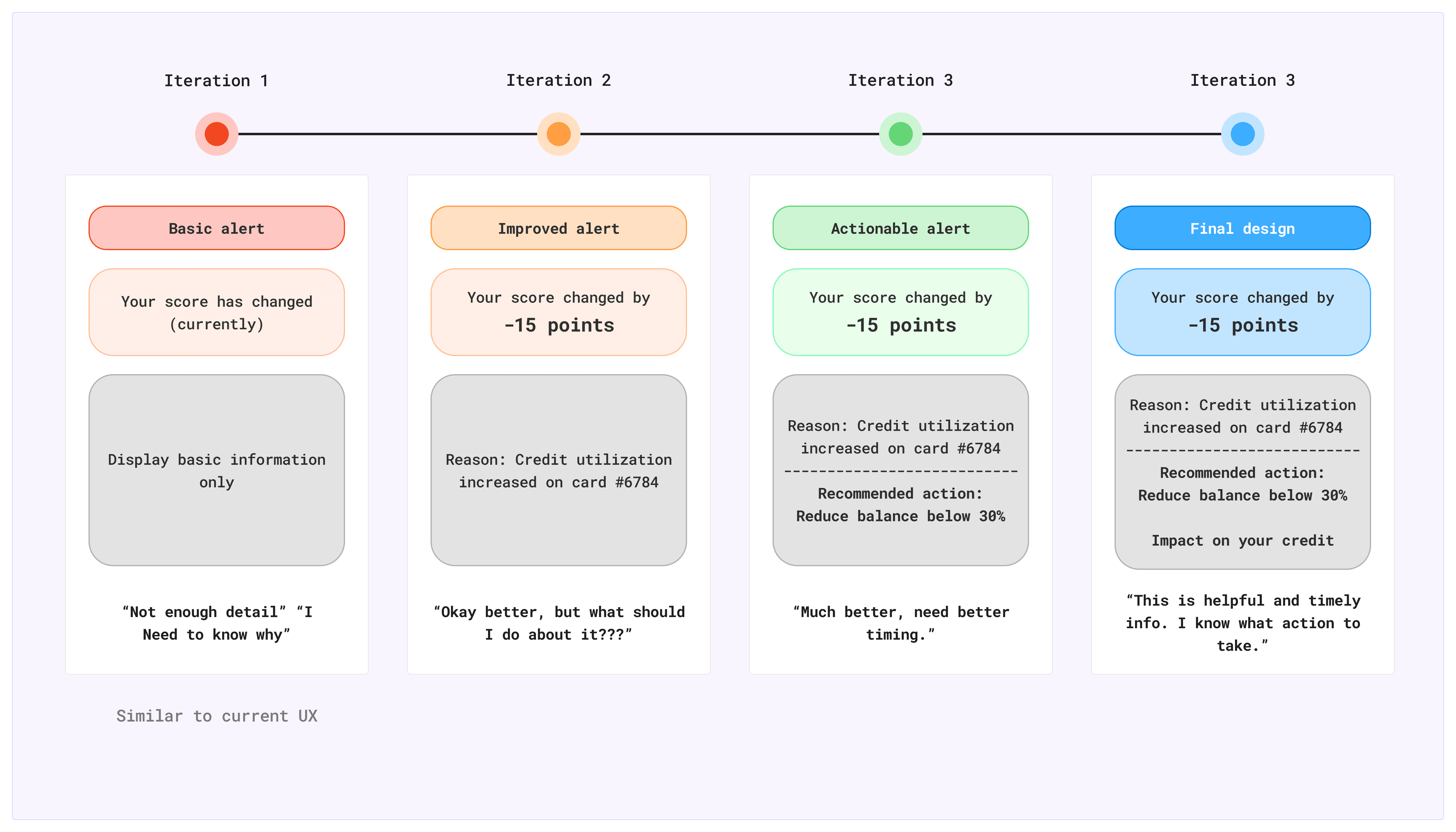

Through extensive research sessions, we uncovered that users needed more than raw data—they required context and clear direction for action. The focus wasn't about just how this feature would look but rather, how we display the alerts to be more insightful. I worked closely with our content strategist to ensure we are providing the right context for each alert. We then tested the copy to 5 users. 5/5 users found the copy updates to be more insightful, engaging, and empathic.

Progressive disclosure: Creating a tiered information architecture that prevented overwhelm while allowing deeper exploration.

Educational structure: Building financial literacy alongside immediate explanations.

Data-driven personalization: Tailoring explanations to each user's specific credit situation.

STEP 04

MVP approach and placement strategy

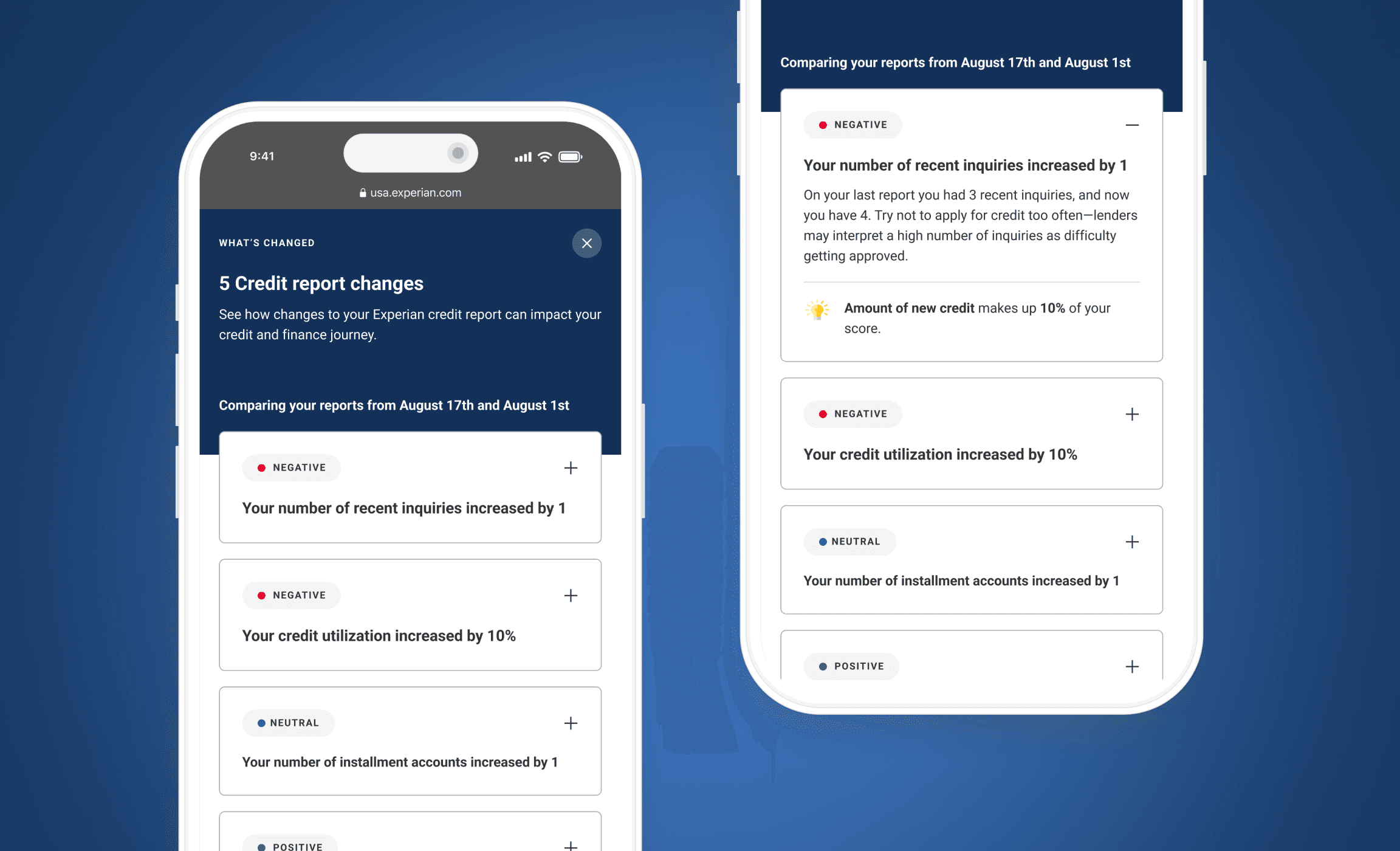

We adopted an MVP approach focused on improving NPS scores with plans to optimize based on results, while conducting traffic audits across the platform to determine optimal placement:

Evaluating the homepage dashboard: First post-login touchpoint

Alerts page: Natural destination after notifications

Report and Scores page: Contextual location for score changes

STEP 05

Iterative design evolution

The design evolved through continuous feedback loops, with each iteration bringing us closer to transforming complex credit data into clear, actionable guidance. We paid particular attention to notification timing and presentation, ensuring users received information when it was most relevant and actionable.

Examples of some of the content we wrote

STEP 06

Controlled deployment and validation

We deployed the feature to a controlled test group to measure impact gathering usage metrics and feedback that demonstrated significant improvements in user comprehension, engagement, and satisfaction before proceeding with full implementation.

Solution

Actionable Credit Score Transparency

The 'What's Changed' feature addresses user frustration by providing clear, actionable insights when credit scores change. The solution transforms complex credit data into easy-to-understand explanations that identify exactly which factors changed, why they matter, and most importantly, what specific actions users can take to improve their scores. By implementing timely notifications across strategic touchpoints in the user journey—primarily on the homepage dashboard with supporting presence on alerts and report pages—the feature creates a transparent experience that empowers users with both knowledge and direction, effectively bridging the gap between technical credit reporting and practical financial management.

Key takeaways

The success of What's Changed demonstrates how simplifying complex financial data into actionable insights, combined with strategic color coding and well-timed notifications, creates a more engaging and understandable experience for users. By delivering personalized insights at the right moment, we empowered users to take control of their credit health with confidence and clarity.

I always design for scale in mind and like to be a couple steps ahead. For future improvements, I wanted to test an experience where the accounts are linked directly to the notifications in the What's Changed feature. This will add even more context and support to what has changed in their report.